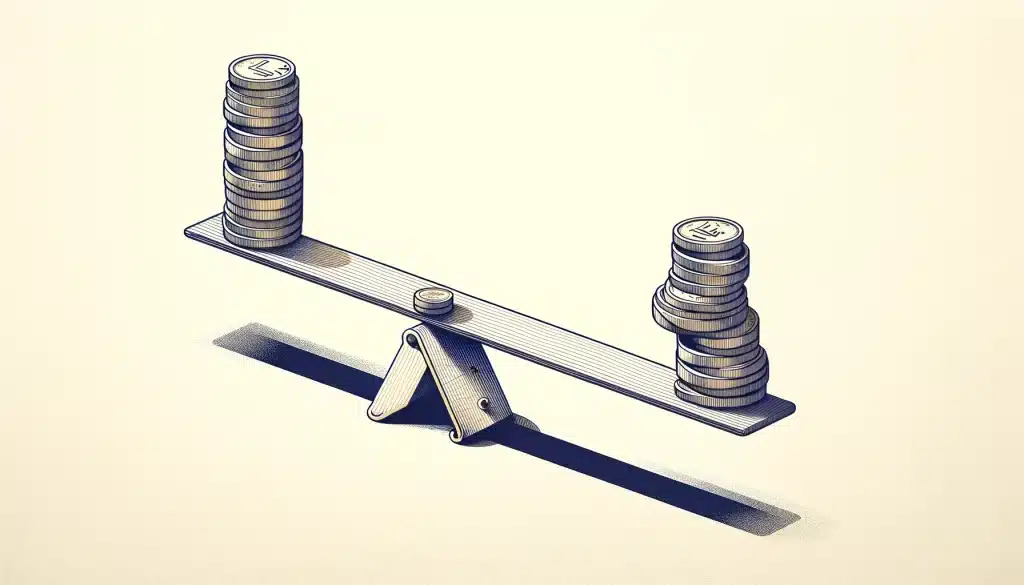

Grasping the nuances of assets vs. liabilities is essential for effective personal finance management. Assets, both tangible like real estate and intangible such as patents, are crucial for generating income and building wealth.

Conversely, liabilities, which include financial obligations like loans and credit card debt, can deplete resources and impact financial health. Understanding the balance sheet—which details assets, liabilities, and equity—highlights their relationship and collective impact on financial stability.

Basically, recognizing the differences between current and long-term liabilities, as well as between tangible and intangible assets, is essential for informed financial planning, saving, and investing. Ultimately, mastering these concepts and managing them wisely paves the way for long-term financial growth and a solid net worth.

Assets include liquid assets like cash, tangible assets such as real estate and vehicles, and intangible assets like patents. They represent the resources with economic value that an individual, company, or country owns. They are expected to provide future financial benefits by generating income, reducing expenses, or appreciating over time. Fixed assets and long-term assets, such as property and equipment, contribute to a company’s assets and are crucial for long-term financial growth.

On the balance sheet, assets are listed alongside liabilities and equity, reflecting the company’s financial standing at a given time. Moreover, total assets, calculated by adding current assets and non-current assets, are instrumental in wealth creation and accumulation. Managing assets effectively involves balancing assets to increase assets’ value and income potential, thereby laying a solid foundation for building robust and positive net worth.

You May Also Like: DINK Lifestyle: How to Get the Most Out of Living Double Income, No Kids

Assets include liquid assets like cash, tangible assets such as real estate and vehicles, and intangible assets like patents. They represent the resources with economic value that an individual, company, or country owns. They are expected to provide future financial benefits by generating income, reducing expenses, or appreciating over time. Fixed assets and long-term assets, such as property and equipment, contribute to a company’s assets and are crucial for long-term financial growth.

On the balance sheet, assets are listed alongside liabilities and equity, reflecting the company’s financial standing at a given time. Moreover, total assets, calculated by adding current assets and non-current assets, are instrumental in wealth creation and accumulation. Managing assets effectively involves balancing assets to increase assets’ value and income potential, thereby laying a solid foundation for building robust and positive net worth.

You May Also Like: DINK Lifestyle: How to Get the Most Out of Living Double Income, No Kids

In personal finance, assets encompass anything that can contribute to an individual’s net worth. Common examples include:

In personal finance, assets encompass anything that can contribute to an individual’s net worth. Common examples include:

The importance of assets in personal finance cannot be overstated, as they play a pivotal role in building wealth, providing financial security, and ensuring a stable future. Assets, by their nature, hold an intrinsic value that can benefit individuals in multiple ways:

The importance of assets in personal finance cannot be overstated, as they play a pivotal role in building wealth, providing financial security, and ensuring a stable future. Assets, by their nature, hold an intrinsic value that can benefit individuals in multiple ways:

Liabilities represent the financial obligations or debts that an individual, corporation, or other entity owes to others. Further, serving as the counterbalance to assets, liabilities play a crucial role in the equation of assets, liabilities, and equity, delineating the obligations that drain resources and could hinder the accumulation of net worth. In personal finance, understanding what are assets vs. liabilities is essential for navigating through financial decisions effectively, as liabilities directly impact one’s financial health and stability, potentially impeding wealth growth.

You May Also Like: How To Save Money In College

Liabilities represent the financial obligations or debts that an individual, corporation, or other entity owes to others. Further, serving as the counterbalance to assets, liabilities play a crucial role in the equation of assets, liabilities, and equity, delineating the obligations that drain resources and could hinder the accumulation of net worth. In personal finance, understanding what are assets vs. liabilities is essential for navigating through financial decisions effectively, as liabilities directly impact one’s financial health and stability, potentially impeding wealth growth.

You May Also Like: How To Save Money In College

In personal finance, liabilities can take various forms, directly impacting an individual’s financial situation:

In personal finance, liabilities can take various forms, directly impacting an individual’s financial situation:

Understanding liabilities is crucial for effective personal finance management, as they significantly impact financial health and wealth accumulation. Liabilities are financial obligations that range from short-term debts like credit card balances to long-term commitments such as mortgages and business loans. Managing these effectively is key to maintaining good financial health and building wealth. These obligations, essential for acquiring assets or covering operational costs, necessitate careful management to avoid compromising financial freedom.

Liabilities impact financial health in several ways:

Understanding liabilities is crucial for effective personal finance management, as they significantly impact financial health and wealth accumulation. Liabilities are financial obligations that range from short-term debts like credit card balances to long-term commitments such as mortgages and business loans. Managing these effectively is key to maintaining good financial health and building wealth. These obligations, essential for acquiring assets or covering operational costs, necessitate careful management to avoid compromising financial freedom.

Liabilities impact financial health in several ways:

Comparing assets vs. liabilities is fundamental to understanding personal finance and the pathway to financial stability and growth. Instead, these two concepts are the pillars upon which the edifice of personal finance is built, each playing a distinct role in shaping an individual’s or entity’s financial health. Here’s a closer look at how assets and liabilities compare and their interconnected roles in financial planning:

Strategies for balancing assets vs. liabilities are essential for anyone looking to achieve financial health and grow their wealth over time. Here are some effective strategies to consider:

Strategies for balancing assets vs. liabilities are essential for anyone looking to achieve financial health and grow their wealth over time. Here are some effective strategies to consider:

Assets vs. Liabilities: What Are Assets?

Assets include liquid assets like cash, tangible assets such as real estate and vehicles, and intangible assets like patents. They represent the resources with economic value that an individual, company, or country owns. They are expected to provide future financial benefits by generating income, reducing expenses, or appreciating over time. Fixed assets and long-term assets, such as property and equipment, contribute to a company’s assets and are crucial for long-term financial growth.

On the balance sheet, assets are listed alongside liabilities and equity, reflecting the company’s financial standing at a given time. Moreover, total assets, calculated by adding current assets and non-current assets, are instrumental in wealth creation and accumulation. Managing assets effectively involves balancing assets to increase assets’ value and income potential, thereby laying a solid foundation for building robust and positive net worth.

You May Also Like: DINK Lifestyle: How to Get the Most Out of Living Double Income, No Kids

Assets include liquid assets like cash, tangible assets such as real estate and vehicles, and intangible assets like patents. They represent the resources with economic value that an individual, company, or country owns. They are expected to provide future financial benefits by generating income, reducing expenses, or appreciating over time. Fixed assets and long-term assets, such as property and equipment, contribute to a company’s assets and are crucial for long-term financial growth.

On the balance sheet, assets are listed alongside liabilities and equity, reflecting the company’s financial standing at a given time. Moreover, total assets, calculated by adding current assets and non-current assets, are instrumental in wealth creation and accumulation. Managing assets effectively involves balancing assets to increase assets’ value and income potential, thereby laying a solid foundation for building robust and positive net worth.

You May Also Like: DINK Lifestyle: How to Get the Most Out of Living Double Income, No Kids

Types of Assets

Assets can be broadly categorized into two main types: tangible and intangible.Tangible Assets

These are physical and material assets that can be seen, touched, and measured. Certainly, tangible assets include real estate properties, vehicles, equipment, inventory, and cash. They are often used for personal use, production of goods, or investment purposes.Intangible Assets

Unlike tangible assets, intangible assets lack physical substance but still hold value due to the rights and advantages they grant the owner. Examples include patents, copyrights, trademarks, software, and brand recognition. Although intangible, these assets can significantly contribute to an individual’s or a company’s value and income generation capability. Read More: How To Invest in Fintech?Examples of Assets in Personal Finance

In personal finance, assets encompass anything that can contribute to an individual’s net worth. Common examples include:

In personal finance, assets encompass anything that can contribute to an individual’s net worth. Common examples include:

Cash and Cash Equivalents

Money in savings accounts, checking accounts, and certificates of deposit. This category of assets is highly liquid, meaning it can be quickly converted into cash without a significant loss in value. This makes it essential for meeting emergency funds and addressing short-term financial needs efficiently.Investments

Stocks, bonds, mutual funds, and retirement accounts like IRAs and 401(k)s. These assets are designed for growth over time, offering potential income through dividends and interest, as well as appreciation in value, contributing to long-term financial security.Real Estate

Primary residences, rental properties, and land. Real estate not only provides a place to live but can also generate rental income and appreciation over time, offering substantial leverage in building wealth.Personal Property

Vehicles, jewelry, art, and other valuable personal items. While not as liquid as cash, these assets can still hold significant value and, in some cases, appreciate over time, such as certain art pieces or collectibles.Business Ownership

Shares in privately owned businesses or entrepreneurial ventures. Also, owning a business or part of it can provide a substantial income source and the opportunity for capital appreciation, reflecting the success and growth of the business. You May Also Like: How Much Should You Save in a Month?Importance of Assets

The importance of assets in personal finance cannot be overstated, as they play a pivotal role in building wealth, providing financial security, and ensuring a stable future. Assets, by their nature, hold an intrinsic value that can benefit individuals in multiple ways:

The importance of assets in personal finance cannot be overstated, as they play a pivotal role in building wealth, providing financial security, and ensuring a stable future. Assets, by their nature, hold an intrinsic value that can benefit individuals in multiple ways:

Income Generation

Many assets, such as investment properties, stocks, and bonds, have the potential to generate income. This income, derived from sources like rent, dividends, or interest, provides a consistent flow of money. It supports an individual’s lifestyle or can be reinvested to further accumulate wealth.Appreciation in Value

Over time, certain assets like real estate and stocks tend to increase in value, known as appreciation. This increase not only boosts net worth but also offers the opportunity to sell these assets for a profit, contributing to financial growth and stability.Financial Security

Assets offer a form of financial security, acting as a safety net in times of economic downturns or personal financial distress. For instance, an emergency fund—considered a liquid asset—can cover unexpected expenses without the need to incur debt.Leverage for Loans

Assets can be used as collateral to secure loans, providing access to funds for various purposes, such as starting a business, investing in education, or purchasing a home. This leverage can be a powerful tool in financial planning and achieving personal goals.Wealth Accumulation and Transfer

Assets are central to the process of wealth accumulation, allowing individuals to build their net worth over time. Additionally, assets can be passed down through generations, contributing to family wealth and financial well-being.Financial Independence

Accumulating assets that generate passive income can lead to financial independence, reducing reliance on traditional employment for income. Generally, this independence opens up opportunities for early retirement, career changes, or pursuing passions without financial constraints. Understanding the importance of assets underscores the need for strategic financial planning and investment. By focusing on acquiring and managing valuable assets, individuals can enhance their financial health, secure their future, and work towards achieving their long-term financial aspirations.Impacts of Assets

Understanding the impact of assets on an individual’s financial health is crucial for effective financial planning and wealth building. Assets, by their very nature, have the potential to generate income, increase in value, and provide financial security. Here’s a closer look at how assets can positively impact financial well-being:Income Generation

Many assets have the inherent ability to produce income. For example, rental properties can generate consistent monthly income through rent payments. Dividend-paying stocks offer regular income through dividend distributions. This ability to create a steady stream of income from assets can significantly enhance an individual’s financial stability and capacity for further investment.Appreciation in Value

Assets like real estate, stocks, and even certain collectibles can be appreciated over time. This appreciation represents an increase in the asset’s worth, which, when realized through sale or disposal, can result in significant capital gains. Appreciation contributes to wealth accumulation, enabling individuals to grow their net worth passively.Leverage for Further Investment

Certain assets can be used as collateral to obtain loans, providing individuals with the leverage to make further investments. This enhances wealth creation by enabling investments in more assets without upfront cash. For instance, real estate equity can secure a home equity line of credit (HELOC). This credit can fund home improvements or further property investments, opening doors to new financial possibilities.Diversification and Risk Management

Investing in a diverse range of assets can spread risk and reduce the impact of volatility on an individual’s portfolio. Diversification across different asset classes (e.g., stocks, bonds, real estate) can protect against significant losses in any one area, ensuring more stable financial growth and security over time.Financial Security and Independence

Assets play a key role in achieving financial security and independence. Accumulating assets that generate passive income can eventually cover living expenses, providing the financial freedom to pursue personal interests, career changes, or retirement. Additionally, owning substantial assets offers a cushion against financial emergencies, reducing reliance on debt and enhancing peace of mind.Legacy and Estate Planning

Assets are central to estate planning, allowing individuals to leave a financial legacy for their heirs. Through careful planning and allocation of assets, individuals can ensure that their wealth supports future generations or causes they care about, extending the impact of their financial achievements beyond their lifetime. Read More: Wanting Vs Needing – When Does Spending Truly Matter?Assets vs. Liabilities: What Are Liabilities?

Liabilities represent the financial obligations or debts that an individual, corporation, or other entity owes to others. Further, serving as the counterbalance to assets, liabilities play a crucial role in the equation of assets, liabilities, and equity, delineating the obligations that drain resources and could hinder the accumulation of net worth. In personal finance, understanding what are assets vs. liabilities is essential for navigating through financial decisions effectively, as liabilities directly impact one’s financial health and stability, potentially impeding wealth growth.

You May Also Like: How To Save Money In College

Liabilities represent the financial obligations or debts that an individual, corporation, or other entity owes to others. Further, serving as the counterbalance to assets, liabilities play a crucial role in the equation of assets, liabilities, and equity, delineating the obligations that drain resources and could hinder the accumulation of net worth. In personal finance, understanding what are assets vs. liabilities is essential for navigating through financial decisions effectively, as liabilities directly impact one’s financial health and stability, potentially impeding wealth growth.

You May Also Like: How To Save Money In College

Types of Liabilities

Liabilities can be classified into two main categories based on their due time:Short-term Liabilities

These are debts or obligations that are due within a short period, typically less than a year. Examples include credit card debt, utility bills, short-term loans, and any other payables due within the year.Long-term Liabilities

Long-term liabilities are financial obligations that are due over a longer period, more than one year. This category includes long-term loans, such as mortgages, student loans, and car loans, as well as other forms of debt like bond repayments. Read More: Essential Criteria Banks Check for Business Loan ApprovalExamples of Liabilities in Personal Finance

In personal finance, liabilities can take various forms, directly impacting an individual’s financial situation:

In personal finance, liabilities can take various forms, directly impacting an individual’s financial situation:

Credit Card Debt

A prevalent form of short-term liabilities, credit card debt occurs when expenditures exceed repayments, accruing interest and increasing the financial burden.Loans

Both short-term and long-term loans (including personal, student, and auto loans) embody business liabilities and personal liabilities, necessitating repayment with interest and influencing the borrower’s financial health.Mortgages

As a significant long-term liability, mortgages represent borrowed funds for purchasing property, requiring regular repayments over time, significantly impacting an individual’s or family’s financial commitments.Medical Bills

Unpaid medical bills, whether due immediately or over time, are also considered liabilities.Unpaid Taxes

Taxes that are due but not yet paid can become liabilities, potentially accruing interest and penalties. You May Also Like: How To Get A Loan And Avoid Loan Scams in 2024Importance of Managing Liabilities

Effectively managing liabilities is critical for several reasons:Credit Score Impact

High levels of debt or mismanaged liabilities can negatively affect your credit score, making it more difficult or expensive to borrow money in the future.Financial Flexibility

Reducing liabilities frees up income that can be redirected towards savings, investments, or spending on personal interests, increasing financial freedom.Reduced Financial Stress

High debt levels can be a significant source of stress and anxiety. Further, managing and reducing liabilities can lead to greater peace of mind.Wealth Building

Minimizing liabilities and focusing on asset accumulation can accelerate the process of wealth building, contributing to financial security and independence. Read More: Zero-based Budgeting – Make use of every dollar to the last cent!Understanding the Impact of Liabilities

Understanding liabilities is crucial for effective personal finance management, as they significantly impact financial health and wealth accumulation. Liabilities are financial obligations that range from short-term debts like credit card balances to long-term commitments such as mortgages and business loans. Managing these effectively is key to maintaining good financial health and building wealth. These obligations, essential for acquiring assets or covering operational costs, necessitate careful management to avoid compromising financial freedom.

Liabilities impact financial health in several ways:

Understanding liabilities is crucial for effective personal finance management, as they significantly impact financial health and wealth accumulation. Liabilities are financial obligations that range from short-term debts like credit card balances to long-term commitments such as mortgages and business loans. Managing these effectively is key to maintaining good financial health and building wealth. These obligations, essential for acquiring assets or covering operational costs, necessitate careful management to avoid compromising financial freedom.

Liabilities impact financial health in several ways:

Decrease in Net Worth

Liabilities directly impact an individual’s net worth, which is calculated as the difference between total assets vs. total liabilities. High levels of debt can significantly reduce net worth, limiting the financial resources available for investment and savings. This reduction in net worth can delay financial goals and impact long-term financial security. They reduce net worth, the difference between total assets and total liabilities, limiting resources available for investments and savings.Interest Expenses

Most liabilities incur interest, which can accumulate over time and increase the total amount owed. High-interest debts, such as credit card debt, can be particularly burdensome, as they can quickly grow and consume a significant portion of an individual’s income. These interest payments represent money that could otherwise be used for saving, investing, or spending on personal needs and goals.Cash Flow Constraints

Liabilities require regular payments, which can restrict cash flow and limit the amount of money available for other uses. Large debt payments can prevent individuals from allocating funds to important financial objectives, such as building an emergency fund, saving for retirement, or investing in assets that could appreciate.Impact on Credit Score

The management of liabilities, including timely payment of debts, influences an individual’s credit score. High levels of outstanding debt or missed payments can negatively affect credit scores, making it more difficult and expensive to obtain financing in the future. A lower credit score can increase the cost of borrowing, further exacerbating financial constraints.Financial Stress

Carrying significant liabilities can lead to financial stress and anxiety, especially if the debt level feels unmanageable. This stress can impact not only an individual’s mental and emotional well-being but also their ability to make clear, strategic financial decisions.Risk of Financial Distress

In cases where liabilities become overwhelming, individuals may face financial distress, including the risk of default, bankruptcy, or foreclosure. Such situations can have long-term consequences for an individual’s financial stability, creditworthiness, and ability to build wealth in the future. Understanding the impact of liabilities underscores the importance of strategic debt management, including prioritizing high-interest debt repayment, maintaining a manageable level of debt, and planning for debt obligations within the broader context of financial goals. By carefully managing liabilities, individuals can minimize their negative impact and enhance their financial well-being and capacity for wealth accumulation. You May Also Like: How to File a Tax ExtensionComparing Assets vs. Liabilities

Impact on Financial Health

The impact of assets vs. liabilities on financial health is profound and multifaceted. Assets serve as a cornerstone for enhancing financial well-being by contributing to an increase in net worth. Moreover, it provides additional income streams through interest, dividends, or rent. Lastly, it offers a layer of financial security that can be leveraged for further investment opportunities or as collateral for borrowing. This positive influence of assets directly contrasts with the role of liabilities. While sometimes, it is necessary for acquiring assets, it require regular outflows of resources to settle. These outflows can significantly constrain financial flexibility. It reduces disposable income and limiting the amount of money available for essential savings or further investment. The balance between these two components—assets vs. liabilities—is critical in shaping an individual’s financial statement. Lastly, it dictates the pace at which financial goals can be achieved. Ultimately, it determines the level of financial stability and growth attainable.Role in Wealth Building

Assets vs. liabilities play contrasting yet interconnected roles in the process of wealth building. Assets represent strategic investments in resources that either appreciate over time or generate income, aiding wealth compounding. They are crucial for enhancing financial portfolios and ensuring long-term growth and stability. Conversely, liabilities, while often necessary for acquiring significant assets like homes via mortgages, require careful management to maintain financial health. Liabilities, while essential for securing assets like homes, must be managed carefully to avoid becoming a wealth barrier. Excessive liabilities increase financial burdens through interest and other costs, limiting the ability to invest in appreciating assets. Therefore, balancing asset growth against the prudent management of liabilities is crucial for securing and enhancing one’s financial future.Management Strategy

Effective financial management involves strategically growing assets and controlling liabilities. The goal is to boost the value and income potential of assets so they not only match but greatly exceed liabilities. This balancing act ensures long-term financial growth and stability. This approach aims at building a robust and positive net worth, laying a solid foundation for financial security and growth. Diversifying assets helps individuals spread risk and access various income sources and capital growth, enhancing financial health. Meanwhile, managing liabilities carefully—through smart debt strategies—protects wealth and ensures that assets achieve their goal of securing a financially prosperous future. This approach is crucial for maintaining financial balance and growth.Long-term Financial Stability and Growth

Maintaining a healthy balance between assets vs. liabilities is crucial for achieving long-term financial stability and growth. This balance ensures that acquiring valuable assets remains the priority, using liabilities strategically to support such acquisitions without over-leveraging. Indeed, the careful planning of liabilities, like loans or mortgages, is crucial. They should enhance your financial portfolio by helping obtain assets that grow in value or generate income, not burden it. Avoiding excessive debt is crucial to avoid financial strain and allow assets to effectively contribute to net worth. A balanced approach lets individuals grow wealth over time while maintaining financial security and flexibility to adjust to changing financial situations. Read More: Conventional Loan Vs FHA LoanStrategies for Balancing Assets and Liabilities

Strategies for balancing assets vs. liabilities are essential for anyone looking to achieve financial health and grow their wealth over time. Here are some effective strategies to consider:

Strategies for balancing assets vs. liabilities are essential for anyone looking to achieve financial health and grow their wealth over time. Here are some effective strategies to consider: